Colocation Take-Up In 2020 To Fall Below 2019 In Europe’s FLAP Market

Colocation take-up is predicted to decrease in 2020 due to Frankfurt and London having their best years in 2018 and 2019.

Amsterdam’s data centre moratorium is another factor that is set to stunt the growth of take-up next year, which will have the potential to bring the numbers down lower than those of 2019, according to newly released figures from CBRE.

Colocation take-up comprises data centre space sold at retailer and wholesaler colocation facilities in the relevant quarter.

However, in the same breath, the figures predict that the four largest European colocation FLAP markets of Frankfurt, London, Amsterdam and Paris are set for a record-breaking finish to 2019, with a “supercharged” last quarter, as enterprise demand in the FLAP markets has increased in the years since 2016.

According to the findings, there was 38MW of take-up and 63MW of new supply across the four markets during Q3.

London and Frankfurt were particularly strong on the demand side, and Amsterdam was responsible for nearly 50% of the new supply. CBRE forecasts that market activity in Q4 will double that of Q3 to create a record year.

Europe is at the centre of the largest data centre M&A transaction on record as Digital Realty announces its intention to acquire Interxion for $8.4bn.

This transaction will combine two of the largest and longest-standing European colocation providers, and in an era of aggressive consolidation across Europe, this transaction stands out in both capital value and footprint terms, according to CBRE.

“These record levels of development underway in the major European markets are creating challenges,” said Mitul Patel, Head of EMEA Data Centre Research at CBRE.

“The availability of freehold land in popular data centre hubs, which offer proximity to large amounts of HV power and fibre routes, such as Slough in the UK and Schiphol in Amsterdam, is highly constrained.

“The effects of these barriers to entry are that data centre developers are either choosing to locate in new, sometimes unproven, locations or are competing aggressively on price for land opportunities.

“Despite cloud providers driving market activity, enterprise demand for colocation remains consistent across the major markets.

“CBRE analysis shows that in the four years from 2016, there has been an average of 43MW of enterprise take-up per year across the four FLAP markets.

“As enterprise companies continue to utilize colocation footprints as part of their hybrid IT architecture, we expect this to remain consistent.”

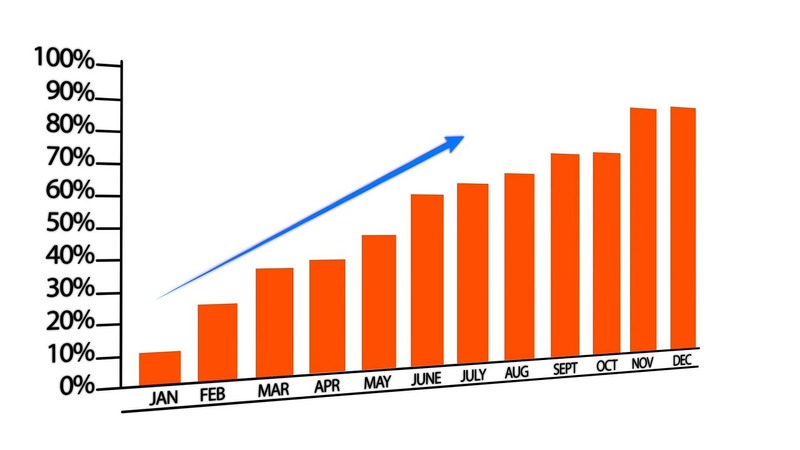

In August this year, the collective take-up of colocation capacity across Europe’s four major datacentre hubs hit record highs in the first six months of 2019, despite a marked slowdown in London, according to CBRE.

Since then, there has been 136MW of take-up in the first three quarters of 2019 across the FLAP markets of Frankfurt, London, Amsterdam and Paris.

Full-year take-up is forecast to surpass 200MW for the first time in history, and CBRE has predicted a further 150MW of new supply in Q4 alone, which would see the year surpass 300MW in new colocation capacity.

By year-end 2019, CBRE forecasts that cloud companies will have been responsible for 80% of the take-up across the four FLAP markets for the second-consecutive year.

source dataeconomy

Industry: Data Centre / Data Center

Latest Jobs

-

- Public Sector Cyber Security Sales | UK

- England

- N/A

-

Public Sector Cyber Security Sales | UK UK | Remote / Hybrid A cyber security provider is seeking a Public Sector Sales professional to drive growth across UK government and public sector organisations. Must have current Cyber Security sales experience. Responsibilities Generate new business selling cyber security solutions into UK public sector Build relationships with CIO, CISO and senior technology stakeholders Manage the full sales cycle from opportunity to contract close Develop pipeline across central government, local government and public sector bodies Support bids, tenders and framework opportunities Experience Proven cyber security sales experience in the UK Track record selling into public sector organisations Familiarity with CCS, G Cloud or other government frameworks Strong stakeholder engagement and deal management skills Location UK based Security Requirements Eligible to obtain UK Security Clearance

-

- Security Architect | MoD - Security Cleared. OUTSIDE IR35 | Hampshire

- N/A

- Outside IR35

-

Security Architect | MOD | Security Cleared | Outside IR35 | Hampshire Commutable The successful candidate must be willing to undergo DV Clearance, ideally already holding active clearance. You will produce high and low level security architecture documentation, guiding and validating designs for systems deployed within sensitive environments. The role requires providing specialist security input into solution design, service transition and change initiatives, working closely with engineering, operations, client and third party stakeholders. You must have current hands on architectural experience, including VMware secure platform design and virtualisation architecture, alongside AWS expertise. This is an outside IR35 contract- 6 month rolling. Part of a longer term MoD project

-

- Active Directory | RBA engineer | UK Remote | SC Clearable

- United Kingdom

- N/A

-

Technical Active Directory (AD) and RBA specialist needed to play a key part in complex, enterprise scale Active Directory and access transformation programmes. You will work alongside senior team, helping reshape access models, modernise legacy directory structures and strengthen security posture across secure environments. This is hands on delivery within high impact projects where your work directly improves access control, compliance and operational resilience. Active UK Security Clearance required. This is a remote role with client travel. Implementation of Role Based Access Control across large AD estates Restructuring complex permission models, security groups and delegated access Supporting domain controller upgrades and core directory improvements Applying security hardening standards and remediating audit findings Enhancing authentication, policy and access governance frameworks Troubleshooting and resolving technical AD challenges within live environments Producing robust technical documentation and identifying project risks You must have the following technical experience Enterprise Active Directory administration Role Based Access and permission remediation OU design and governance Group Policy management Security group delegation models DNS and DHCP services Kerberos authentication / NTLM PowerShell scripting and automation Azure AD | Entra ID Hybrid identity environments Identity Governance PAM

-

- Identity and Access Management Consultant (Saviynt & Microsoft Entra) | UK

- United Kingdom

- N/A

-

Role summary Technical IAM consultant delivering identity governance and cloud identity solutions to enterprise clients. What you will do Implement / Configure / Deploy Saviynt IGA / Microsoft Entra solutions: Lead technical workshops, gather requirements and translate into solution designs. Troubleshoot complex issues, support testing and deployments. Produce technical artefacts and configuration guides. Key skills Hands-on Saviynt IGA experience (workflow, connectors, access governance). Strong practical knowledge of Microsoft Entra ID / Azure AD identity and access controls. Understanding of identity protocols (SAML, OAuth, OpenID Connect) and hybrid identity. Experience with APIs / REST for integrations and automation. What we are looking for Proven delivery experience in IAM / IGA projects, preferably in consulting. Confident communicator with client-facing delivery exposure.